A Complete Guide to Buying Diamonds Through diamond 247

Games |

2025-10-03 18:12:23

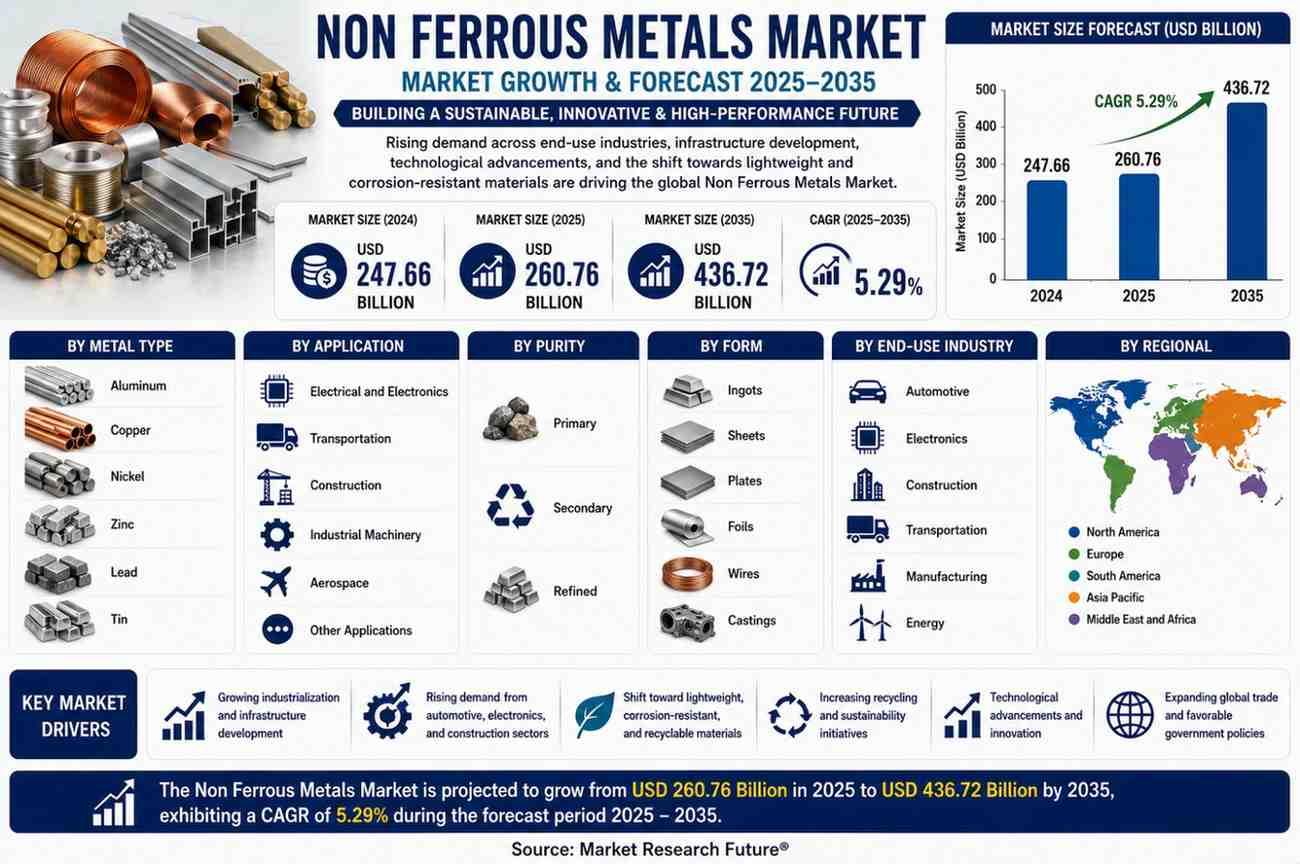

According to Market Research Future®, the Non Ferrous Metals Market was valued at USD 247.66 billion in 2024 and is projected to grow from USD 260.76 billion in 2025 to USD 436.72 billion by 2035, registering a compound annual growth rate (CAGR) of 5.29% during the forecast period (2025–2035). The market is being shaped by accelerating investments in electric mobility, renewable energy infrastructure, sustainable manufacturing, and advanced industrial production. Increasing emphasis on recyclable materials, lightweight engineering solutions, and secure supply chains is expected to sustain demand for non-ferrous metals throughout the forecast period.

Non-ferrous metals have become indispensable to modern industrial development because they combine excellent electrical conductivity, corrosion resistance, lightweight performance, and high recyclability. Aluminum, copper, nickel, zinc, lead, and tin support critical manufacturing activities across transportation, construction, electronics, aerospace, telecommunications, energy, and industrial machinery. Their widespread use in emerging technologies further reinforces their strategic importance within the global economy.

Rapid urbanization and industrialization continue driving large-scale infrastructure projects that require significant volumes of aluminum products, copper wiring, structural alloys, and specialized industrial metals. At the same time, governments worldwide are implementing energy transition policies that encourage investments in renewable electricity generation, battery manufacturing, electric vehicles, and modern transmission networks. These developments are expanding the consumption of non-ferrous metals across both mature and emerging markets.

In parallel, manufacturers are increasing investments in recycling systems, energy-efficient refining technologies, and environmentally responsible mining practices to address resource security concerns while meeting increasingly stringent environmental regulations.

The Non Ferrous Metals Market reached USD 247.66 billion in 2024 and is estimated to grow to USD 260.76 billion in 2025.

With a projected CAGR of 5.29%, the market is expected to attain approximately USD 436.72 billion by 2035, reflecting sustained expansion across global manufacturing, infrastructure development, transportation, and clean energy industries.

The market continues to benefit from multiple long-term growth drivers.

Electrification across transportation systems is significantly increasing demand for copper, aluminum, and nickel used in electric vehicles, charging infrastructure, battery technologies, and electrical components.

Large-scale renewable energy installations require extensive quantities of conductive metals for wind turbines, solar power systems, transmission cables, substations, and grid modernization projects.

Infrastructure development programs across emerging economies continue supporting demand for aluminum extrusions, copper products, galvanized steel coatings containing zinc, and industrial castings.

Growing consumer electronics production further expands metal consumption through smartphones, laptops, wearable devices, communication equipment, and semiconductor manufacturing.

Increasing focus on sustainability has also accelerated investments in secondary metal production and closed-loop recycling systems that reduce dependence on virgin raw materials.

Asia-Pacific remains the largest regional market due to rapid industrialization, expanding automotive production, electronics manufacturing, and government infrastructure investments. Countries throughout the region continue strengthening domestic manufacturing capabilities while increasing renewable energy capacity and transportation infrastructure.

North America benefits from modernization of power grids, rising electric vehicle production, aerospace manufacturing, and investments in critical mineral supply chains.

Europe continues emphasizing low-carbon manufacturing, circular economy initiatives, advanced recycling technologies, and sustainable industrial production. The region's environmental regulations are encouraging greater use of recycled aluminum, copper, and other non-ferrous metals across multiple industries.

South America remains a strategically important mining region with abundant copper and other mineral resources, while the Middle East and Africa continue attracting investments in mineral exploration, extraction, refining, and export infrastructure.

Expanding electric vehicle manufacturing will continue increasing demand for lightweight metals and battery materials.

Renewable energy projects provide long-term opportunities for aluminum and copper suppliers.

Modernization of aging electrical infrastructure supports higher consumption of conductive metals.

Technological innovations in recycling improve resource efficiency while lowering production costs.

Growth in aerospace manufacturing encourages development of advanced lightweight alloys.

Industrial automation and digital manufacturing increase demand for precision-engineered non-ferrous metal products.

Sustainability remains one of the industry's defining trends as producers focus on reducing carbon emissions through renewable-powered smelting facilities, energy-efficient refining processes, and improved recycling technologies.

Digital transformation is improving productivity across exploration, mining, refining, logistics, and inventory management through artificial intelligence, automation, predictive maintenance, and real-time operational analytics.

Manufacturers are increasingly developing advanced alloy compositions that deliver improved mechanical strength, corrosion resistance, thermal conductivity, and lightweight performance for next-generation industrial applications.

Supply chain diversification has also become a strategic priority as companies seek to reduce geopolitical risks while improving long-term raw material security.

The global market remains highly competitive, with leading companies continuously investing in operational efficiency, resource expansion, technological innovation, and sustainability initiatives.

Major participants including Alcoa Corporation, Rio Tinto, BHP Group, Glencore, Southern Copper Corporation, and First Quantum Minerals Ltd. continue strengthening their global positions through mine expansion projects, advanced processing facilities, digital mining technologies, recycling investments, and strategic partnerships across downstream manufacturing industries.

Research into low-carbon production methods, high-performance alloy development, and environmentally responsible extraction techniques is expected to remain central to competitive differentiation over the coming decade.

The Non Ferrous Metals Market is expected to experience stable long-term expansion as industrial electrification, infrastructure modernization, clean energy deployment, and advanced manufacturing continue reshaping global demand patterns. Increasing investments in recycling infrastructure, responsible mining, automation, and digital technologies will further improve operational efficiency while supporting environmental sustainability objectives.

With the market forecast to grow from USD 260.76 billion in 2025 to USD 436.72 billion by 2035 at a CAGR of 5.29%, industry participants that prioritize innovation, supply chain resilience, and sustainable production practices will remain well positioned to capture emerging opportunities across global markets.